What is a Spendthrift Clause?

Almost any family can benefit from an estate plan. Estate planning typically includes a trust, a will, and several other options to protect assets and provide for beneficiaries long after we are gone. It can provide a great sense of comfort to families to know what to expect during and after one’s life by stipulating where the assets will be transferred to. An “extra” protection clause or provision is a spendthrift clause.

A spendthrift clause or provision can provide extra protection from two different angles regarding a trust. The first is that it ensures that the beneficiary can’t “waste” or disperse too much of their assets at once. It also allows for the protection of those assets from any creditors of the beneficiary.

How Does the Spendthrift Clause Protect Assets Within the Family?

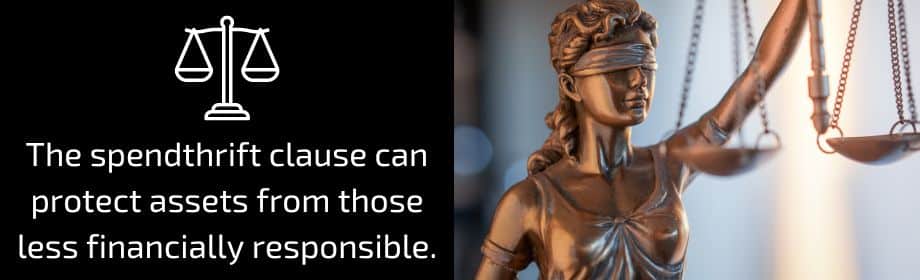

The spendthrift clause can protect assets from those less financially responsible. For example, perhaps you are setting up a trust stipulating where your assets will be transferred upon death. You have two children. One of which is much less financially responsible than the other.

It may concern you that your child may “blow through” the assets or not make decisions that can sustain the assets you are prepared to transfer. This clause allows for specific verbiage to direct limitations of the beneficiary’s control, assuring that they will have to follow the instructions you provided for how they manage the assets.

How can the Spendthrift Clause Protect Assets from Creditors?

For example, your two children will inherit $50,000 each upon your death. If one of your children has $20,000 in credit card debt, a creditor can request that the $20,000 debt be satisfied through the trust assets. The trustee, however, can simply deny this request citing the spendthrift clause.

Assets listed within the spendthrift clause are protected while they remain in the trust’s property. Once those assets are dispersed, however, they become available to creditors.

What are the Exceptions to the Spendthrift Clause?

There are a few exceptions to the spendthrift clause. The first is if the beneficiary owes child or spousal support that the courts have ordered. The assets included in the trust (and stipulated through the spendthrift clause) would not be protected as they would be used to satisfy any court-ordered support owed.

A judgment creditor may also have provided services to protect a beneficiary’s interest in the trust’s assets. In this case, the funds associated with those funds would not be protected through the spendthrift clause.

The third exception is regarding any claim the state of Florida or the United States may have against the trust assets. This exception is not black and white, as it is unclear what claims the law refers to. Unpaid or past-due taxes may be included in this category as an exception to the spendthrift clause.

How Do I Create a Spendthrift Clause?

As part of a comprehensive estate plan, you can include a spendthrift clause in your trust. It requires specific verbiage about how the assets are managed. You can work with an estate attorney to ensure that your wishes are thoroughly explained within the clause.

A spendthrift clause is only enforceable if it requires both the voluntary and involuntary transfer of assets. It is crucial to ensure that the spendthrift clause is worded accurately for this reason.

When is a Spendthrift Clause Most Beneficial?

Chances are, if you have taken the time to include a trust in your estate planning, it can also be beneficial to include a spendthrift clause. There are some instances, however, when it can be imperative to have.

Such examples are if one or more of the trust’s beneficiaries are prone to making poor financial decisions. If they are easily duped or make poor choices in investments or spending, this clause can provide them with protection. You can still include them in the trust but have added insurance for how or when the funds are dispersed to protect the beneficiary from themselves.

Suppose one or more of the beneficiaries has addictive tendencies. This can be difficult to foresee, as some individuals don’t present with addictive tendencies until they have substantial money to spend on their addiction. Whether it be gambling, drugs, or alcohol, there may not be addictive tendencies in their lives before an inheritance, but an inheritance combined with them grieving a significant death may lead to addictive choices. In this case, it can be a “better safe than sorry” approach to include the spendthrift clause.

Why Work With an Attorney?

There are some situations where having a do-it-yourself approach to estate planning may work well for your family. If your estate is straightforward or the assets are limited, you may find it best to handle the estate planning independently.

As with most things in life, estate management or planning rarely is black and white. It can be incredibly beneficial to you and your family to work with an experienced attorney who is well-versed in all things estate planning. They can work closely with you to determine all assets have been discussed and consider things you may have yet to think of, as making plans for your estate isn’t likely something any of us will need to do more than once.

A comprehensive estate plan can provide us peace of mind long after we are gone and extra support and protection for our loved ones.

Contact our office today at (407) 904-9166 to learn how we can best assist you with your estate planning needs.